Follow the money. We analyze global VC investment flows into the toy sector, revealing the hottest trends from AI companions and edutainment to the circular economy and immersive play.

Venture capital is a powerful leading indicator of where an industry is heading. In 2026, the flow of smart money into the toy and play sector reveals a clear map of the future. Investors are no longer funding just the next fad doll or plastic brick; they are strategically backing companies that sit at the intersection of play, technology, sustainability, and deep consumer experience. This capital is fueling a fundamental redefinition of what a toy can be.

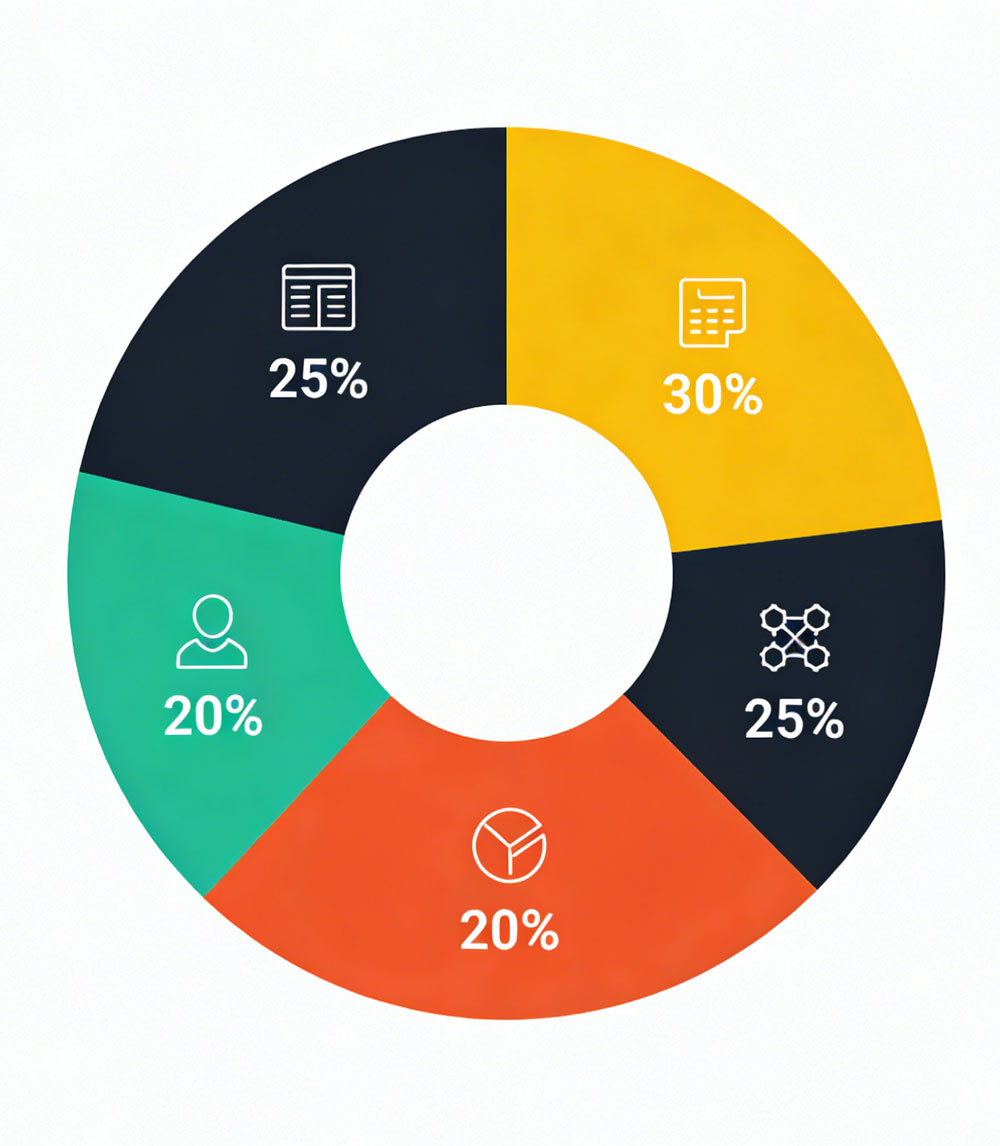

Hot Investment Categories for 2026

The AI & Robotic Companion Stack: As covered in our first article, this remains

the dominant theme. Investment is flowing not just into consumer product companies, but into the underlying technology stack: startups specializing in emotional AI algorithms, low-cost sensor fusion, child-safe voice interaction engines, and durable, expressive actuation for robotic pets and characters.

Edutainment 2.0 – “Stealth Learning” Platforms: The line between learning and play is dissolving. VCs are backing digital platforms and subscription services that use engaging gameplay, personalized adaptive learning paths, and rich narratives to teach coding, math, language, and socio-emotional skills. The key is that the educational outcome is a byproduct of compelling fun.

The Circular Toy Economy: Sustainability is a major investment thesis. Startups creating toy subscription/rental models, certified refurbishment platforms, and innovative materials (like truly biodegradable bio-plastics or mycelium-based packaging) are attracting significant capital. Investors see a massive opportunity in helping the industry transition from a linear “take-make-dispose” model to a circular one.

Immersive & Phygital Play Experiences: This category blends digital and physical. It includes:

AR-Enhanced Toys: Physical toys that unlock digital games, stories, or creative tools when viewed through a smartphone or AR glasses.

Location-Based Entertainment: Ventures creating immersive, themed play spaces that integrate interactive projections, sensor-driven environments, and physical play elements, offering a high-value out-of-home experience.

UGC Creation Tools: Platforms that allow kids to easily design, customize, and even 3D print their own toy characters or accessories, tapping into the creator economy.

The Investor Mindset: What VCs Are Looking For

Today’s toy investors are not passive. They seek:

Strong Founder Vision: Teams with a unique insight into the future of play, often blending

expertise in tech, gaming, and child development.

Recurring Revenue Models: A move away from one-off toy sales toward subscriptions (D2C boxes), software-as-a-toy updates, or platform-based marketplaces that generate predictable, long-term revenue.

Defensible Technology or IP: A proprietary AI model, a patented material process, or a deeply engaging original IP universe that creates a competitive moat.

Clear ESG Alignment: A business model that inherently addresses environmental or social goals is now table stakes for many top-tier funds.

Implications for the Broader Industry

This influx of venture capital is a rising tide that lifts all boats. It:

Accelerates R&D, bringing cutting-edge tech from labs to playrooms faster.

Attracts Top Talent, pulling software engineers, data scientists, and sustainability experts into the toy sector.

Raises Consumer Expectations, teaching a new generation that toys can be intelligent, responsive, and environmentally responsible.

For established toy companies, this means the competitive set is no longer just other toy makers—it includes agile tech startups. Partnerships, acquisitions, and internal corporate venture arms are becoming essential strategies to harness this innovation wave. In 2026, the toy industry is unequivocally a tech-and-impact-driven growth sector in the eyes of global investors.

Post time: Apr-15-2026